目前我持有日馳的股票,前段時間噴高高,但最近不停漲停!跌停!搞的我心力交瘁。於是今天決定用一個數學模型來預測可能的崩盤時機。

LPPL是我之前在ricequant看到的泡沫預測模型,對於那些極右側交易者(追漲)滿有幫助的,然而這個模型只考慮股價,不考慮財報、月報等,所以比較適合用在大盤,個股可能比較沒辦法。但我還是很想知道日馳是否要崩盤了!?XD

預防針

這邊還是要提醒大家,這個只是個有趣的小實驗,但我真的不確定這個很可靠,請不要依賴LPPL買賣股票,可以當作一個參考,追蹤一下日馳的股價是否跟LPPL模型顯示的一樣。我個人是持非常懷疑的態度!請大家不要因為這篇文章來決定要不要買日馳。說不定明天就崩到底給你看XDD。

LPPL

該網站都已經寫的滿清楚的,我就不多加贅述,雖然你第一次看可能會不太懂,可以先看以下的補充說明:一些關於model(模型)的觀念:

model就是一個數學模型,由一或多個數學公式組成,可以拿來預測天氣、預測人口成長率、預測各種東西,是個很強大的東西!

LPPL就是一個數學震盪公式:

當中的一些變數:

- y(t):模擬的股價 1. t:就是指每天的日期

- tcrash:崩盤的日期 3. x:其它一些比較不重要的參數

我們的目標就是調整 tcrash 和 x 的值,讓模擬的股價 y(t) 可以對應到某支股票的實際股價 ym(t),就可以了。通常我們會用以下的方法對應到一個股價:

這個步驟就是調整參數,讓股價跟模型預測的股價趨近一樣,通常也可以稱為最佳化!

於是,我們就有了 tcrash 的值,也就可以預測崩盤的時機了!

接下來可以參考網站中的介紹,看一下LPPL的預測能力。

以下示範日馳給大家看:

取得日馳股價

首先我們用 pandas 中的 datareader,取得日馳的股價

from pandas_datareader import data # pip install pandas_datareader

import matplotlib.pyplot as plt # pip install matplotlib

import pandas as pd # pip install pandas

%matplotlib inline

data = data.DataReader("1526.tw", "yahoo", "2017-04-01","2018-01-10")

c = data['Close']

c.plot()最佳化

接下來,將網站中的LPPL複製過來,並且將日馳的股價 data.Close assign給 sz 這個變數。

這段code是在計算最佳參數,我沒有仔細閱讀code。有時寫程式就要學會複製貼上,可以用,就好了,對我們來說這不是科學問題,而是工程問題XD。

LPPL模型分析

import numpy as np

import matplotlib.pyplot as plt

from scipy.optimize import fmin_tnc

import random

import pandas as pd

from pandas import Series, DataFrame

import datetime

import itertools

sz = data.Close

date = sz.index

time = np.linspace(0, len(sz)-1, len(sz))

close = np.array(np.log(sz))

DataSeries = [time, close]

def lppl (t,x): #return fitting result using LPPL parameters

a = x[0]

b = x[1]

tc = x[2]

m = x[3]

c = x[4]

w = x[5]

phi = x[6]

return a + (b*np.power(tc - t, m))*(1 + (c*np.cos((w *np.log(tc-t))+phi)))

def func(x):

delta = [lppl(t,x) for t in DataSeries[0]]

delta = np.subtract(delta, DataSeries[1])

delta = np.power(delta, 2)

return np.sum(delta)

class Individual:

"""base class for individuals"""

def __init__ (self, InitValues):

self.fit = 0

self.cof = InitValues

def fitness(self):

try:

cofs, nfeval, rc = fmin_tnc(func, self.cof, fprime=None,approx_grad=True, messages=0)

self.fit = func(cofs)

self.cof = cofs

except:

#does not converge

return False

def mate(self, partner):

reply = []

for i in range(0, len(self.cof)):

if (random.randint(0,1) == 1):

reply.append(self.cof[i])

else:

reply.append(partner.cof[i])

return Individual(reply)

def mutate(self):

for i in range(0, len(self.cof)-1):

if (random.randint(0,len(self.cof)) <= 2):

self.cof[i] += random.choice([-1,1]) * .05 * i

def PrintIndividual(self):

#t, a, b, tc, m, c, w, phi

cofs = "A: " + str(round(self.cof[0], 3))

cofs += "B: " + str(round(self.cof[1],3))

cofs += "Critical Time: " + str(round(self.cof[2], 3))

cofs += "m: " + str(round(self.cof[3], 3))

cofs += "c: " + str(round(self.cof[4], 3))

cofs += "omega: " + str(round(self.cof[5], 3))

cofs += "phi: " + str(round(self.cof[6], 3))

return "fitness: " + str(self.fit) +"\n" + cofs

def getDataSeries(self):

return DataSeries

def getExpData(self):

return [lppl(t,self.cof) for t in DataSeries[0]]

def getTradeDate(self):

return date

def fitFunc(t, a, b, tc, m, c, w, phi):

return a - (b*np.power(tc - t, m))*(1 + (c*np.cos((w *np.log(tc-t))+phi)))

class Population:

"""base class for a population"""

LOOP_MAX = 1000

def __init__ (self, limits, size, eliminate, mate, probmutate, vsize):

'seeds the population'

'limits is a tuple holding the lower and upper limits of the cofs'

'size is the size of the seed population'

self.populous = []

self.eliminate = eliminate

self.size = size

self.mate = mate

self.probmutate = probmutate

self.fitness = []

for i in range(size):

SeedCofs = [random.uniform(a[0], a[1]) for a in limits]

self.populous.append(Individual(SeedCofs))

def PopulationPrint(self):

for x in self.populous:

print(x.cof)

def SetFitness(self):

self.fitness = [x.fit for x in self.populous]

def FitnessStats(self):

#returns an array with high, low, mean

return [np.amax(self.fitness), np.amin(self.fitness), np.mean(self.fitness)]

def Fitness(self):

counter = 0

false = 0

for individual in list(self.populous):

print('Fitness Evaluating: ' + str(counter) + " of " + str(len(self.populous)) + " \r"),

state = individual.fitness()

counter += 1

if ((state == False)):

false += 1

self.populous.remove(individual)

self.SetFitness()

print("\n fitness out size: " + str(len(self.populous)) + " " + str(false))

def Eliminate(self):

a = len(self.populous)

self.populous.sort(key=lambda ind: ind.fit)

while (len(self.populous) > self.size * self.eliminate):

self.populous.pop()

print("Eliminate: " + str(a- len(self.populous)))

def Mate(self):

counter = 0

while (len(self.populous) <= self.mate * self.size):

counter += 1

i = self.populous[random.randint(0, len(self.populous)-1)]

j = self.populous[random.randint(0, len(self.populous)-1)]

diff = abs(i.fit-j.fit)

if (diff < random.uniform(np.amin(self.fitness), np.amax(self.fitness) - np.amin(self.fitness))):

self.populous.append(i.mate(j))

if (counter > Population.LOOP_MAX):

print("loop broken: mate")

while (len(self.populous) <= self.mate * self.size):

i = self.populous[random.randint(0, len(self.populous)-1)]

j = self.populous[random.randint(0, len(self.populous)-1)]

self.populous.append(i.mate(j))

print("Mate Loop complete: " + str(counter))

def Mutate(self):

counter = 0

for ind in self.populous:

if (random.uniform(0, 1) < self.probmutate):

ind.mutate()

ind.fitness()

counter +=1

print("Mutate: " + str(counter))

self.SetFitness()

def BestSolutions(self, num):

reply = []

self.populous.sort(key=lambda ind: ind.fit)

for i in range(num):

reply.append(self.populous[i])

return reply;

random.seed()

from matplotlib import pyplot as plt

import datetime

import numpy as np

import pandas as pd

import seaborn as sns

sns.set_style('white')

limits = ([8.4, 8.8], [-1, -0.1], [350, 400], [.1,.9], [-1,1], [12,18], [0, 2*np.pi])

x = Population(limits, 20, 0.3, 1.5, .05, 4)

for i in range (2):

x.Fitness()

x.Eliminate()

x.Mate()

x.Mutate()

x.Fitness()

values = x.BestSolutions(3)

for x in values:

print (x.PrintIndividual())別懷疑,就給它跑下去就對了,我也沒仔細看就跑了,需要跑一段時間。

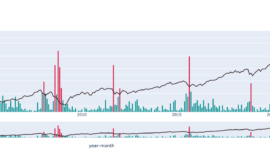

跑完後應該會得到下圖:

可以看到這段代碼總共做了3次預測,以防算出來不準,其中的 critical time 就是指崩盤日期,約在380天左右,而我們總共測了200天,所以距離今天(2018-01-10),大概還需要 380 – 200 = 180 個交易日,才會有毀滅性的崩盤。

最後畫出圖,我也是複製貼上:

data = pd.DataFrame({'Date':values[0].getDataSeries()[0],'Index':values[0].getDataSeries()[1],'Fit1':values[0].getExpData(),'Fit2':values[1].getExpData(),'Fit3':values[2].getExpData()})

data = data.set_index('Date')

data.plot(figsize=(14,8))

結論

LPPL這個模型看看就好,財報、月報也很重要,依照這個程式的結果,日馳距離泡沫崩盤還要很久,但千萬別因為這樣就買入,畢竟股票有太多要考量的因素了,大戶的脾氣不是數學模型可以模擬的XDDDDDDD…。

{kind=link}

{kind=link}

{kind=link}